Uniswap Monthly Financial Report & Analysis - Feb. 24

This report covers the performance of the Uniswap Protocol and UNI token leading up to and including February 2024.

Table of Contents

Executive Summary

Multichain (Volume, Liquidity, Fees)

Market Share (Volume, Liquidity, Fees)

Layer1 vs Layer2 (Volume, Liquidity, Fees)

Second-Order Values (Protocol Efficiency, Fee Rates, Protocol Yield)

UNI Token

Executive Summary

In February 2024, the Uniswap Protocol processed $45.73 billion in monthly volume (-1.9%) across $5.98 billion in liquidity (+37.4%), earning market makers $91.36 million in fees (+29.1%).

Across all chains, Ethereum saw the most Uniswap volume with $27.3 billion in v3 pools, seconded by Arbitrum. Base saw the highest month-over-month growth in volume, liquidity, and fees.

This month, the protocol experienced a relative decline in volume of -0.5% over competing DEX protocols, with a 1.4% relative increase in liquidity and a staggering 7.5% increase in fees generated.

Layer 2 deployments received 27.4% of all Uniswap volume, down from 34.7% in January. Layer 2 liquidity remains steady at 11.5% of the total, generating 13.4% of fees, down from last month.

Multichain

Highlighting activity across each major chain with a Uniswap deployment, this section informs on the absolute growth of the Uniswap Protocol and the relative growth across multiple chains.

Only chains with high-quality API data are included.

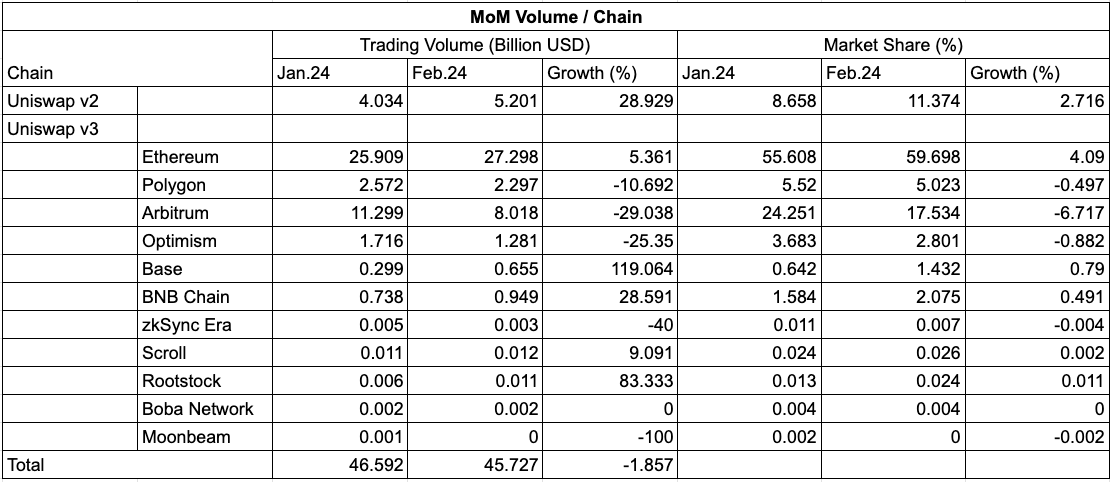

Volume

Over the past three months, Uniswap protocol volume has remained consistent. It’s interesting to note that volume has not increased alongside recent token prices.

In February, although total protocol volume remained consistent, nine of the twelve chains saw at least a 10% change in volume. Base was the biggest winner, marking a 119% increase, whereas Moonbeam volume fell to negligible values, displaying a 100% decrease.

Uniswap’s largest Layer 2 deployments all underperformed, with Polygon (-10.7%), Arbitrum (-29%), and Optimism (-25.4%) seeing large volume falls compared to January 2024.

Relatively, Uniswap v3 on Ethereum saw the biggest increase in market share, growing 4.1% to a 59.7% share of total protocol volume. Uniswap v2 grew its market share by 2.7%, partially due to the multichain launch this month but likely due to the recent memecoin surge onchain.

Liquidity

Uniswap liquidity surged 34.7% to the highest levels this year, with Uniswap v2 and v3 on Ethereum accounting for the bulk of the growth. As liquidity is denominated in dollars, we can attribute a good portion of the gain to price increases throughout the ecosystem.

Every Uniswap deployment saw liquidity growth in February, with all but Moonbeam seeing 10%+ growth. The biggest increases were Rootstock and Base, with 624% and 314% increases, respectively. Market share amongst chains remained relatively stable, with no changes greater than one percent in either direction.

With incentives going live shortly, thanks to the Uniswap Revitalization and growth proposal, we can expect to see further liquidity growth on newer Uniswap v3 deployments.

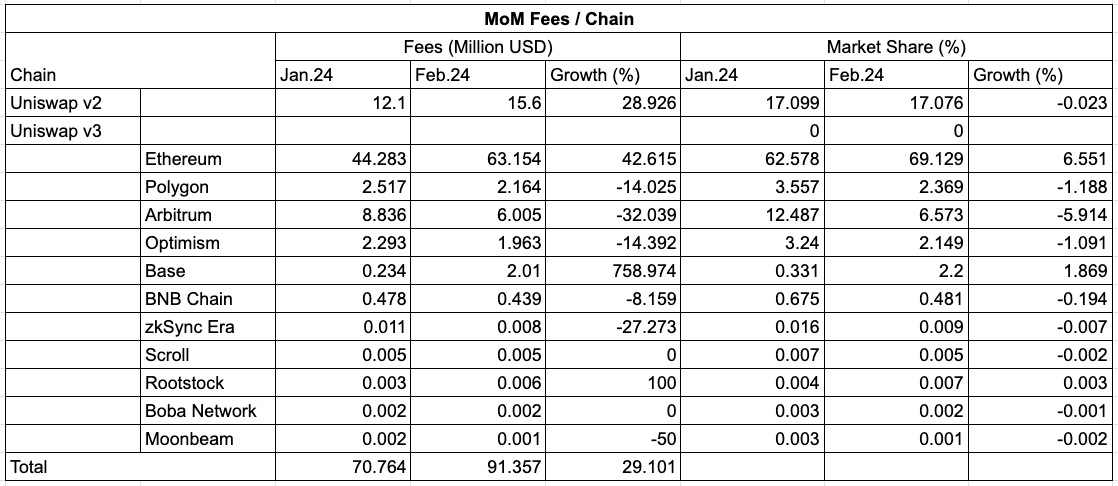

Fees

The Uniswap protocol paid liquidity providers more fees in February than any other month in the past year. LPs earned a total of $91.4m in fees, a 29.1% increase from January 2024. With volume remaining stable month over month, we can deduce that volume has moved to higher fee pools, primarily in Uniswap v3 on Ethereum.

Along with volume, Uniswap v3 on Polygon, Arbitrum, and Optimism underperformed in fees accrued compared to January 2024. Arbitrum specifically saw a $2.8m fall in fees, losing 5.9% in market share.

Month over month, the best performer was Base, which grew from $234k in fees to $2.01m, marking a 759% increase. The Ethereum deployment grew its fees by $18.9m in the month of February, which is more than any other deployment accrued all month.

Market Share

This section highlights Uniswap Protocol's success against leading competitors. To be considered a competitor, the protocol must be a spot DEX with at least one deployment on a chain alongside Uniswap v3. To filter out the data, the spot DEX must have a minimum February 2024 volume of $1 billion.

Pancakeswap, Curve, Camelot, TraderJoe, Quickswap, Balancer, and Maverick meet this criterion.

Volume

Uniswap’s market dominance remained steady from January to February, making up 59% of DEX volume amongst qualifying competitors.

While Uniswap remained steady over the month, other DEX protocols saw large swings in volume. Camelot volume fell 32.7% and lost 1.1% market share. On the other hand, Quickswap grew 51.4%, and Balancer experienced a 28.6% increase.

Liquidity

As mentioned above, the DEX ecosystem as a whole saw large liquidity increases, likely due to prices trending upwards in February. Uniswap outperformed competitors by claiming an extra 1.4% market share, bringing its liquidity share to 45.2%.

Uniswap, Balancer, Curve, and Quickswap all had 30%+ liquidity increases in the short month of February, performing the best in the set. Each DEX did have growth; however, Maverick’s was only 6.7%, underperforming the nearest competitor by a factor of 2.3x.

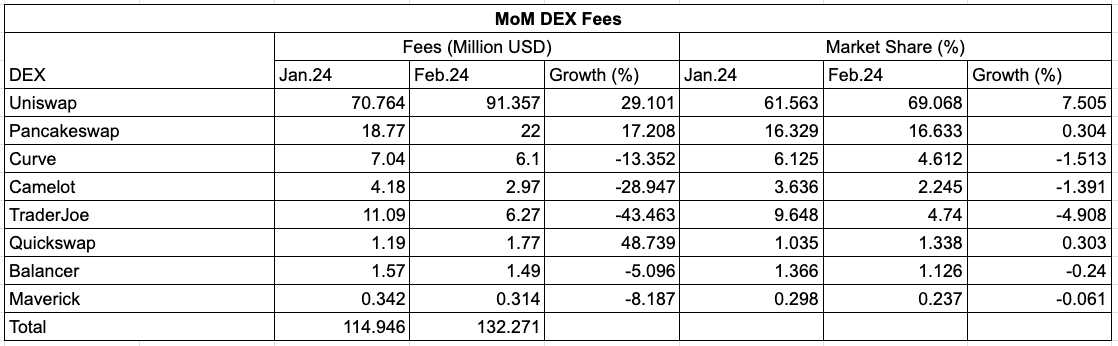

Fees

From a fee perspective, Uniswap dominated its aggregated competitors in February. As mentioned above, Uniswap distributed $91.4m in fees last month, increasing its share of the fee market to 69.1% from January’s 61.6%.

TraderJoe liquidity providers had the worst month, with fees nearly being cut in half at a 43.5% decrease. Uniswap and Quickswap LPs had the largest increases in fees earned at 29.1% and 48.7% respectively.

Layer 1 & Layer 2

This section explores the changes in Uniswap Protocol activity between Layer 1 and Layer 2 deployments as a percentage of total activity. Only Uniswap v2 and v3 on Ethereum are counted as Layer 1 deployments, with Polygon, Optimism, Arbitrum, Base, zkSync, Scroll, Rootstock, and Boba making up the Layer 2 grouping.

Volume

After Layer 2’s best month yet in January, Layer 1 reclaimed a good portion of Uniswap volume, now sitting at 72.6% of the total. As the bull market progresses, we’ll watch how these values shift.

Liquidity

February was another stale month for Uniswap Layer 1 / Layer 2 liquidity, staying at an 88.5%/11.5% split. Regardless of volume and price action, liquidity has yet to migrate. We’ll see how these values shift as Uniswap liquidity incentives go live on Layer 2 deployments.

Fees

Along with volume, Layer 2 fee collection took a relative hit in February 2024. With all the volume flowing through high-fee pools on Ethereum, this divergence was expected. For Layer 2 fee collection to catch up, high-fee pools would need to start processing volume on Layer 2 and not exclusively Uniswap v2 and v3 on Ethereum.

Accounting for differences in liquidity, Layer 2 liquidity providers still earn 1.28x more per dollar deposited.

Second-Order Values

We analyzed the second-order values of the Uniswap Protocol against those of its competitors. These data sets divide Uniswap v2 and v3 to highlight the differences in design and outcome.

Protocol Efficiency

Protocol efficiency is measured by dividing the total volume by the total liquidity - finding how much volume is generated per dollar of liquidity.

The competing DEXs form three distinct tiers. Maverick still maintains the highest protocol efficiency by a large margin in a group of its own. Uniswap v3, Camelot, TraderJoe, and Quickswap are in the next tier between a 10x and 20x volume-to-liquidity multiplier. The poorest performers in this category are Uniswap v2, Pancakeswap, Curve, and Balancer, with multipliers less than 8x.

Month over month, there is a decrease in this metric, with liquidity values outpacing volume.

Fee Rates

The average fee rate is measured by dividing fees by volume - determining the fee rate on each dollar of volume.

Uniswap v2 maintains the highest fee rate at 0.3%, as expected. Maverick retains the lowest fee rate among the DEXs, likely due to its liquidity incentives, which are not accounted for in fees collected. Uniswap v3 increased its fee rate in February, led by the Ethereum deployment, as mentioned above.

Protocol Yield

A protocol’s yield is found by dividing fees by liquidity - displaying the monthly return per dollar deposited.

Uniswap v3’s liquidity providers earn an average of 2% per month, around 3x the earnings of v2 depositors. Curve and Balancer providers earn a low 0.2% and 0.1%, respectively, making them the worst liquidity destinations in the group. TraderJoe tops the list at 3.2% monthly returns for providers.

UNI Token

The Uniswap Protocol's governance token, UNI, performed very well in February against the industry’s benchmark assets, BTC and ETH, even though the benchmarks increased by 45% and 49% in February. UNI nearly doubled its returns at a 93% increase.

The significant leap on the charts came on the day of the Uniswap Foundation’s temperature check, proposing a large-scale upgrade to Uniswap protocol governance by enabling UNI stakers and delegators to earn protocol fees.

Compared to the competition, Uniswap’s UNI token outperformed once again. Most DEX tokens performed similarly to BTC and ETH within the +29.8 to +47.86 range, with Maverick’s MAV being the clear loser, down 20.9% in February.

The data from this report was sourced from the Oku API, Oku Analytics, DeFiLlama, and TradingView charting. Subscribe to the newsletter for the March report and more updates on the performance of the Uniswap Protocol across chains and against competitors.