Uniswap Monthly Financial Report & Analysis - September ‘24

This report covers the performance of the Uniswap Protocol and UNI token leading up to and including September 2024.

Table of Contents

Executive Summary

Multichain (Volume, Liquidity, Fees)

Market Share (Volume, Liquidity, Fees)

Layer1 vs Layer2 (Volume, Liquidity, Fees)

Second-Order Values (Protocol Efficiency, Fee Rates, Protocol Yield)

UNI Token

Executive Summary

In September 2024, the Uniswap Protocol processed $40.18 billion in monthly volume (-27.4%) across $5.57 billion in liquidity (+7.5%), earning market makers $61.72 million in fees (-11.1%).

Across all chains, Ethereum saw the most Uniswap volume with $20.77 billion in v3 pools, seconded by Arbitrum. Each of the major deployments experienced significant decreases in volume and fees.

This month, the protocol experienced a relative decline in volume (-2.9%) and liquidity (-1.7%) over competing DEX protocols, with a slight increase in fees (+0.4%).

Layer 2 deployments’ share of volume and fees fell this month, while their liquidity share rose for the first time since May 2024.

This month, the recent Uniswap v3 deployments on Polygon zkEVM and Lisk were added to the report.

Multichain

This section highlights activity across each major chain with a Uniswap deployment and informs on the absolute growth of the Uniswap Protocol and its relative growth across multiple chains.

Only chains with high-quality API data are included.

Volume

Uniswap protocol volume dropped significantly this month, down 27.4% to $40.18 billion. This is the lowest monthly volume since October 2023.

Volume declines were felt across the board in September, with each of the five largest deployments experiencing 30%+ drawdowns. The Uniswap v3 deployment on Sei was the only one to grow its volume, increasing 44.5% from $78 million to $113 million. Surprisingly, Uniswap v2 managed to maintain its volume, only falling 0.6% on the month. In the past, volume declines were felt more by the storied protocol, given its use for memecoins and other longtail assets.

With all major v3 deployments seeing declines, Uniswap v2 grew its protocol market share by 4.9%, now accounting for 18.1% of all volume.

Liquidity

After a large falloff in August, Uniswap protocol liquidity bounced back in September, growing 7.5% to $5.57 billion across all deployments. September is the first month with liquidity growth since May of this year.

The largest deployments all experienced an increase in liquidity, with the exception of Arbitrum (-9.0%). Uniswap v3 on Base had the largest liquidity inflow by a large margin, more than doubling its TVL to $265.00 million. Taiko marked the largest outflows, with liquidity falling 81.5% as UNI and TAIKO incentives expired on the chain.

Base also experienced the largest growth in liquidity market share at 2.3%, half of which came directly from Uniswap v2. The CPAMM protocol experienced liquidity growth this month, but not enough to keep up with the v3 deployments.

Fees

Protocol fees fell in September, alongside volume decreases, with the protocol paying the lowest amount to liquidity providers so far in 2024.

As expected, fees across the multichain deployments followed the volume figures. The exception to the rule is Uniswap v3 on Ethereum, which only saw a fee decline of 9.7% despite a 30.6% decrease in volume, highlighting that volume shifted slightly towards higher fee-tier pools in September.

Uniswap v2 grew its fee market share by another 3.8%, now accounting for over a third of the Uniswap protocol’s total fee distribution.

Market Share

This section highlights Uniswap Protocol's success against leading competitors. To be considered a competitor, the protocol must be a spot DEX with at least one deployment on a chain alongside Uniswap v3. To filter out the data, the spot DEX must have a consistent monthly volume of $1 billion.

Pancakeswap, Curve, Camelot, TraderJoe, Quickswap, Balancer, and Aerodrome meet this criterion.

Volume

Uniswap’s volume dominance declined once again in September. Although both Uniswap and the competitor set experienced fall-offs, Uniswap’s was much larger (27.4% vs 18.5%).

Every DEX in the competitor set experienced a volume fall-off in September amidst the poor market conditions. The best performer was Pancakeswap, only marking a 7.8% decline in volume, growing its share of the pie by 3.7%. The worst performer was Camelot, losing $1.95 billion in monthly volume, a shocking 42.4% fall-off.

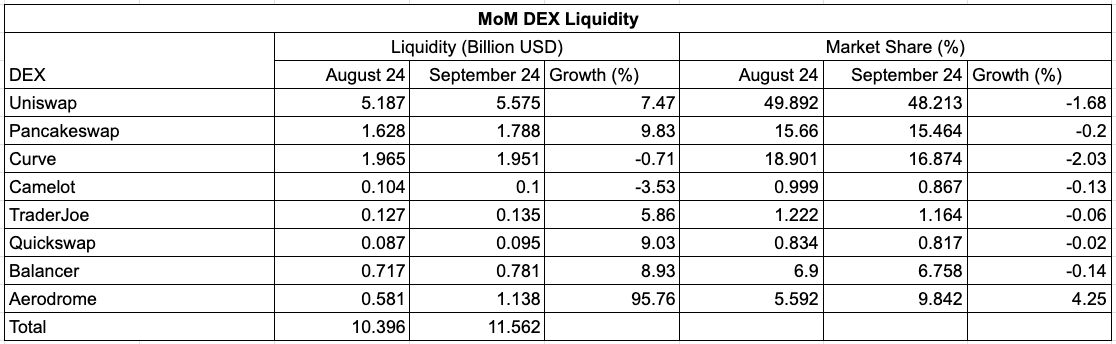

Liquidity

After dipping below 50% of liquidity last month for the first time in 2024, the Uniswap protocol continued to lose market share against the competitor set. Although TVL increased, TVL on competing DEXs increased faster.

Many of the major DEXs saw growth in liquidity figures, but Aerodrome was by far the biggest destination for new positions. Aerodrome TVL nearly doubled from $581m in August to $1.14 billion in September. The Base DEX now accounts for nearly 10% of all liquidity in the competitor set.

Despite increasing liquidity by 7.5% in September, the Uniswap protocol lost 1.7% of its market share, with market share from every DEX flowing to Aerodrome.

Fees

Fees fell across the board in September, leading the Uniswap protocol to maintain its market share in fee distribution at 63.4%.

With large volume drop-offs in September, only Uniswap and Pancakeswap were able to weather the storm for their liquidity providers, maintaining a similar amount of fee collection and distribution at -11.1% and -2.8% respectively. Curve, Camelot, TraderJoe, and Balancer each distributed less than 70% of the prior month’s fees.

From a market share perspective, Pancakeswap was the biggest winner growing its share of fees by 2.2% to 24.5% - nearly a quarter of all fees in the competitor set.

Layer 1 & Layer 2

This section explores the changes in Uniswap Protocol activity between Layer 1 and Layer 2 deployments as a percentage of total activity. Only Uniswap v2 and v3 on Ethereum are counted as Layer 1 deployments, with Polygon, Optimism, Arbitrum, Base, zkSync, Scroll, Rootstock, Linea, Blast, Manta, Boba, Taiko, Sei, Mantle, Polygon zkEVM, Lisk and Moonbeam making up the Layer 2 grouping.

Volume

Layer 2’s volume share fell slightly in September, now at 28.4% of the total. This is the lowest level since February of 2024.

Liquidity

Layer 2’s liquidity share grew slightly in September, further highlighting that liquidity doesn’t directly follow volume.

Fees

Layer 2’s share of fees tumbled by 4.6% in September, implying that higher fee-tier volume occurred on Layer 1 in September.

Second-Order Values

We analyzed the second-order values of the Uniswap Protocol against those of its competitors. These data sets divide Uniswap v2 and v3 to highlight the differences in design and outcome.

Protocol Efficiency

Protocol efficiency is measured by dividing the total volume by the total liquidity - finding how much volume is generated per dollar of liquidity.

Protocol efficiency fell across the board in August, with liquidity rising and volume falling across most protocols. In percentage terms, Aerodrome had the biggest falloff this month, as liquidity increased 95.8% and volume fell 9.8%. Camelot’s concentrated liquidity protocol still facilitates the most volume per dollar in TVL.

Fee Rates

The average fee rate is measured by dividing fees by volume, determining the fee rate per dollar of volume.

Uniswap v2 maintains the highest fee rate at 0.30%, as expected. The remainder of the fee rates remained relatively flat, with a slight bump in Uniswap v3 fee rates, now at 0.12% across all pools.

Protocol Yield

A protocol’s yield is found by dividing fees by liquidity - displaying the monthly return per dollar deposited.

Liquidity providers across the major DEXs performed much worse in September then they did in August. Not only was there a decline in fee revenue, but liquidity increased across the board. This month, Aerodrome liquidity providers earned a 0.5% return on average, down significantly from August’s 1.3%. Most of the major DEXs offered an average return of between 0.9% and 0.14%, with the exceptions being Curve and Balancer as usual.

UNI Token

The Uniswap Protocol's governance token, UNI (+22.1%) had a great month in September, outperforming ETH (+0.9%) and the industry’s largest asset, BTC (+6.1%).

Uniswap’s UNI token was the second-best performer this month, with only Aerodrome’s AERO token (+91.6%) performing better. Interestingly, last month, the three worst performers were AERO, BAL, and UNI - each marking a big comeback in September.

September token performance was certainly more correlated to the protocol’s TVL than their volume figures.

The data from this report was sourced from the Oku API, Oku Analytics, DeFiLlama, and TradingView charting. Subscribe to the newsletter for the October report and more updates on the performance of the Uniswap Protocol across chains and against competitors.